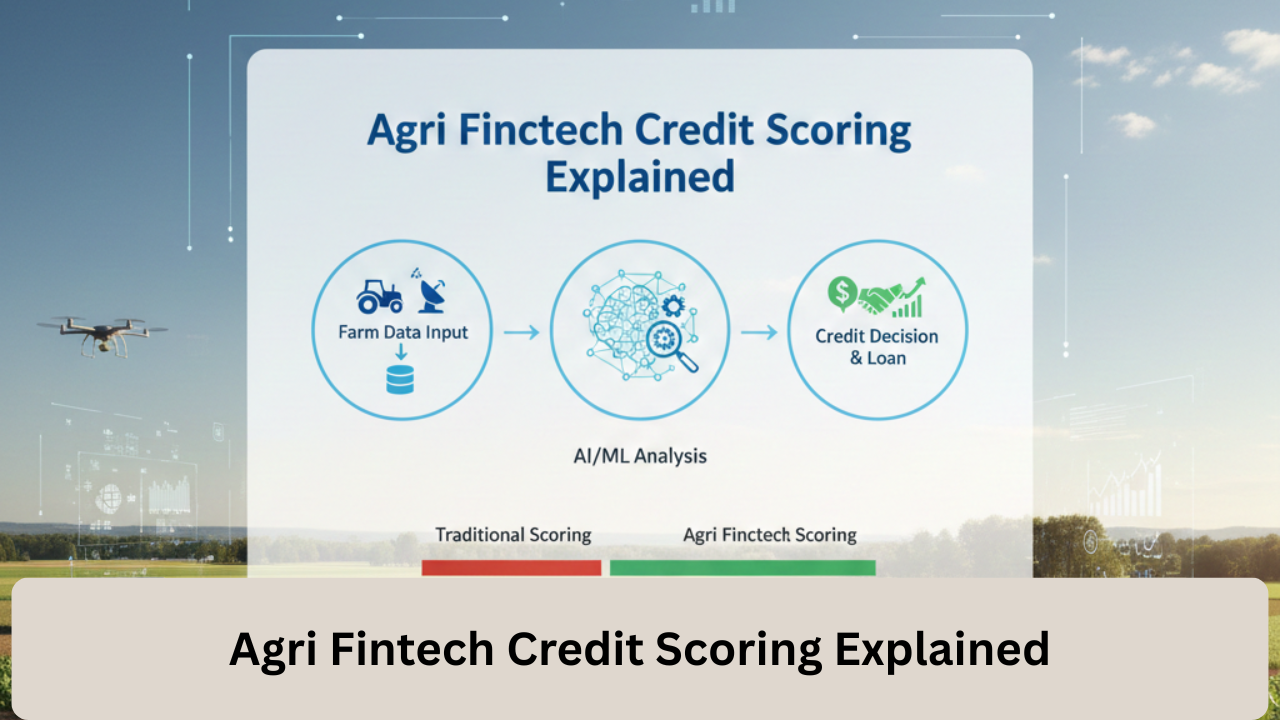

Agri fintech is an emerging industry due to the rapid digitalization of agriculture and entails the combination of financial technology with agricultural processes to increase access to capital, efficiency, and sustainability. One of the most significant innovations in the sphere addressed to agri fintech credit scoring.

Traditional credit screening processes are likely to overlook the fact of smallholder farmers and agribusiness, the majority of which lack formal financial records. Agri fintech credit scoring is a solution to fill this gap by offering different data, sophisticated analytics, and technically based models for superior and more inclusive creditworthiness.

It is grounded on the idea that agri fintech credit scoring generates the agricultural data points designed to evaluate farmers terms of their ability to repay the loans and risk profile. This may be crop rotations, weather, soil quality, satellite pictures, records of transactions, and even phone call history. These variables combined can assist fintech platforms in offering more personalized finance goods.

Knowing Four Principles of Credit Evaluation

The conventional 4 Rs of credit-score evaluation are rather applicable in agri fintech lending and nonetheless tend to complemented with digital tools. These instructions help the lenders in familiarizing themselves with the general risk profile of the borrower. The first R is Repayment capacity which is the capacity of the borrower to repay a loan in regard to the expected income.

This is achieved the agricultural sector through crop yield analysis, commodity prices, and seasonal cash flows. Predictive analytics enable Fintech platforms to forecast more accurately in terms of predicting the volatility of income and repayment schedule. The second R is the Risk bearing ability that examined.

The ability of the farmer to be able to withstand a shock such as droughts, floods, or a fall in prices. The agri-fintech solutions tend to bundle climate and insurance cover in order to reach resilience to these risks. The third R is return potential, which involved with the viability of the activity that is being financed. By examining the productivity of farms, input efficiency, and the market.

The Key Approaches that Wield a Credit Rating

The credit score is not obtained because of a single factor but many factors, which related to each other. In the case of agri fintech, they have adjusted to suit agricultural borrowers without reducing good risk management practices.

- The first one is payment behavior, which is a pointer of consistency with which a borrower fulfills his/her financial obligations. In the example of farmers, it may be repayment of a loan that occurred previously, input credit, or even utility and mobile bills.

- The second one is the credit exposure and it the aggregate of the number of debts owed. Agrifintech platforms monitor outstanding loans across multiple lenders to prevent over-indebtedness, a major challenge in rural finance globally today.

- The third is credit history length, which establishes the time a borrower has been active in financial projects. Sales records and cooperative membership histories from wallets can help fintech firms estimate financial experience despite limited banking ties.

- The fourth one is the credit diversity that presupposes the usage of different financial products. A farmer who has successfully dealt with different types of funding, such as the working capital loans and equipment financing, regarded as averse to risk because he or she has a position to deal with finances.

Building Blocks of Credit Score: 7 Essentials

Besides those of high level, credit scoring models often built on smaller ones. In the case of agri fintech, there seven fundamental building blocks that usually considered to formulate elaborate credit profile.

- The first block is the stability of income that measures predictability and stability of farm incomes. Crop diversification and the presence of different markets used to increase this.

- The latter is production performance, regarding the trends of yield, the input efficiency, and the optimal farming practices. In this regard, sensors, satellites, and farm management application data are critical.

- The third one is the market access and it assesses how easily the farmers are able to sell their produce. It also reduces uncertainty of the income and increases creditworthiness due to good relations with the buyers, cooperatives, or online markets.

- The fourth block cost structure, which investigates the input cost, cost of labor, and efficiency operation. These aspects applied by Regions Fintech to find profit margins and the ability to repay.

- The fifth is possession of properties such as land use rights, machinery, or livestock. Other assets provide additional security, though not required as collateral, signaling long-term commitment and sustained investment in farming activities.

- Is this conversation helpful so far? The sixth building block is risk mitigation mechanisms such as crop insurance, contract farming arrangements, or government support. These mechanisms lessen the chances of default and the trustworthiness of the lenders heightened.

- The final block is the digital behavior, which entails mobile behavior, frequency of transaction, and engagement with digital space. The knowledge will help fintech companies to find reliability and transparency data- Unaided.

A smarter future of Agricultural Finance

As the problems with agriculture increasingly becoming numerous due to climate change, with a population that becomes more and more numerous and financial markets unstable, the role of intelligent credit assessment cannot overestimated. Agri fintech credit score is a paradigm shift of financial services to the realities of modern-day agriculture.

A combination of data and technology and agricultural knowledge creates an inclusive and more resilient financial ecosystem. Lastly, the innovation does not only provide access to capital by farmers but also improves the whole agricultural value chain that paves the way to sustainable development in the nation and long-term rural prosperity.